Goliath Resources: Evaluating Surebet’s Real Ceiling

From 4–6Moz Assumptions to a 10Moz Question

This morning’s Goliath release is not about a new zone. It’s about value density and system maturity.

The company recalculated 54 previously reported holes into gold equivalent grades and showed that including silver and other payable metals increased overall grade value by an average of 13.2% versus gold-only reporting.

For several years, Goliath’s narrative centered on high-grade gold intercepts. The underlying assays always included multi-element data, but the market largely digested the project as a gold story. This shift toward AuEq formalizes what was already present in the rock: Surebet is a polymetallic system with meaningful payable credits.

However, that 13.2% uplift applies to that 54-hole dataset. It cannot automatically be applied across all historical drilling. Surebet is a layered system with multiple lodes and zones. Metal ratios vary. The correct takeaway is not “everything is 13% better,” but rather “value per tonne is consistently stronger than gold-only framing suggested.”

The larger point is structural.

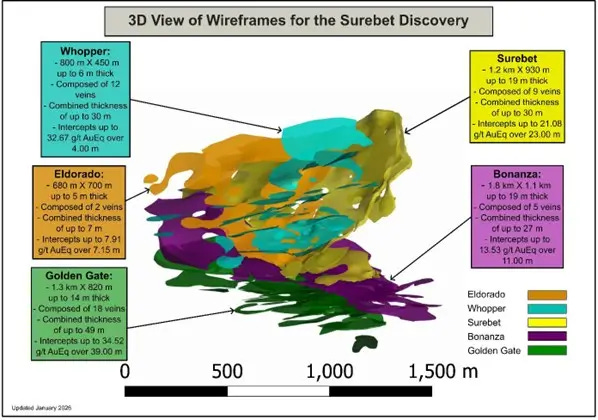

Goliath now describes Surebet as comprising five main gold-rich zones and 46 mineralized lodes, supported by over 1,500 pierce points, with a 100% mineralization hit rate in the holes reported to date. Those are statistically significant data points in any exploration system, particularly in a structurally complex district like the Golden Triangle… and expansion remains central.

The company drilled over 64,000 meters in 2025 and continues to deliver a similarly scaled 2026 program. That scale of drilling, combined with persistent hit rates, suggests the geological model is increasingly predictive. Expansion both laterally and vertically is what ultimately determines whether this becomes a contained high-grade core or a district-scale multi-million-ounce system.

At this stage, geometry matters as much as metallurgy.

On metallurgy, there is already a baseline. Published test work has shown strong gold recoveries — approximately 92% via gravity and flotation, with nearly half of the gold recovered through gravity alone. The company has emphasized a benign metallurgical profile. That baseline de-risks the early narrative considerably.

The next step in metallurgy is not “prove it works.” It’s “prove it works across zones and at scale.” But that is now running parallel to expansion, not ahead of it.

Valuation is where this becomes interesting.

A pre-resource company trading near the C$400 million range is not being priced as a one-million-ounce project. The market is implicitly assigning probability to a multi-million-ounce outcome. Something in the 4–6 million ounce conceptual range is rational given drilling density and footprint to date.

The question is whether the geometry supports something larger.

A 10 million ounce system grading 4–5 g/t would imply roughly 60–100 million tonnes of mineralized material. That requires sustained strike, real widths, vertical continuity, and consistent grades across expanding zones. That outcome depends primarily on expansion success — not metallurgy at this point.

Large discoveries are rare. Even one million ounces is statistically uncommon globally. Multi-million-ounce systems are rarer still. But the Golden Triangle is one of the few districts where multiple large deposits coexist along the same structural corridor. That geological context provides precedent.

This release refines the economic framing and reinforces the structural coherence of the system. It does not change the stage of development overnight. The core drivers remain expansion, density, and conversion of footprint into defensible volume.

The story is tightening.

Continuity remains strong.

Expansion remains the key driver of upside.

Metallurgy has a credible baseline and now needs scaling, not validation from zero.

The next major re-rating will come from continued expansion that begins to clearly support a resource pathway — not from incremental improvements in recovery assumptions.

That’s where the real leverage sits.

Disclaimer:

This analysis is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. The views expressed are based on publicly available information and reasonable assumptions as of the date of publication. Mineral exploration involves significant risk, including geological, technical, financing, and market risk. There is no guarantee that exploration results will lead to a defined resource, economic study, or mine development. Readers should conduct their own due diligence and consult with a licensed financial advisor before making any investment decisions.